Accounting in the 1C program: “Enterprise Accounting 3.0” is based on the correct completion of various reference books. One of the most important directories is the “Cost Items” directory. It contains information for maintaining analytical accounting for, namely: 08; 20; 23; 25; 26; 28; 29; 44. Each of these accounts has a subaccount of the same name:

This subconto reflects only turnover; there are no balances in the “Cost Items” subconto.

Correct filling this guide is especially important, since it participates in and influences the correct formation of financial statements of the enterprise.

To go to the directory, go to the “Directories” menu, then in the “Income and Expenses” section, select the “Cost Items” link. The directory list form will open.

Initially, when you first start the program, even with a clean infobase, the directory will be filled with default values, or so-called predefined elements. They are marked with an icon. These articles cannot be deleted and are not recommended to be changed, as they will most likely be changed to their original value when the configuration is updated.

Important! In any case, it is not recommended to change anything in any cost item if accounting has already begun for it. If such a need arises, you need to repost the documents where transactions involving expense accounts were generated.

Get 267 video lessons on 1C for free:

The “Cost Items” directory is the same for all cost accounts.

To enter a new cost item, click the “Create” button. The form for creating a new directory element will open.

When entering the name of a new item, it is advisable not to split similar costs, but to group them into one element. This will prevent the directory from becoming bloated. For example, if an enterprise uses corporate cellular communications, has landline phones, and IP telephony, you should create one cost item - “Communication Services”.

I advise you to plan the cost structure of the enterprise in advance, so that later there is no confusion and you do not have to repeatedly correct and retransmit documents.

The “Type of expense” detail is mandatory, and it is important to fill it out correctly, since the income tax return is filled out item by item. Accordingly, tax accounting is carried out in the context of expense items.

The “Default Use” attribute shows the purpose of the article and is filled in when it is necessary for it to be automatically inserted into the selected document.

Here is an example of filling out the cost item “Write-off of materials”:

Any accountant knows that a directory system is used to maintain records in the 1C accounting program. In this article we will stop and take a closer look at one of them, the so-called “Cost Items” directory*, as well as cost accounts, their classification and setup using the example of working with one of the most popular accounting solutions - 1C: Accounting 8.3.

*Cost items are a division by type of cost to analyze the composition of the expenditure of funds.

To attribute expenses in accounting, the following expense accounts are used: 20, 23, 25, 26, 29, 44, 91. All of them are intended to summarize information.

Let's specify which one:

20/Main production: data on the costs of main production. The debit of this account includes direct expenses associated with the production of main products, work performed, and services provided. This also includes indirect costs from accounts 25 and 26, and the costs of completed auxiliary production from account 23

23/Auxiliary productions: information on the costs of auxiliary production.

25/General production expenses: information on the costs of servicing the organization’s main and auxiliary production facilities.

26/General expenses: generalized administrative expenses not directly related to the production process.

29/Servicing industries and farms: data on costs incurred by service industries and farms.

44/Sales expenses: expenses associated with the sale of products, goods, works and services.

91/Other income and expenses: respectively.

At the same time, these accounts can be used to maintain analytical accounting* by cost items.

*Analytical accounting is accounting that is kept in accounts accounting and allows you to group detailed information about business transactions. It is carried out in cost and physical indicators.

To maintain analytical accounting on cost accounts, the program uses various directories: cost items, divisions, item groups, other income and expenses.

The subconto “cost item” to accounts in 1C is necessary to separate by type of expense. It is used in accounting to analyze the composition of costs, and is also used for the purposes of tax accounting and classification of expenses by type of NU costs.

For cost accounts: 20, 23, 25, 26, 29, 44 in 1C is used single directory"Cost Items". For analytical accounting of other income and expenses, the reference book “Other income and expenses” is used.

On account 20 (as well as 23 and 29), analytical accounting is carried out by divisions (subconto “divisions”), types of products (subconto “item groups”) and types of costs (subconto “cost items”).

On accounts: 25, 26, 44, analytical accounting is carried out by divisions and types of costs.

If we are talking about 91 accounts, then we can add that analytical accounting is kept on it by types of other income and expenses.

Moreover, each division, each type of product and each type of cost is an element of the corresponding directory.

In 1C Accounting 8.3, analytics for an account look like this (for example, for account 20.01):

In order to open the directory, you need to go to the menu: Directories - then to the Income and Expenses section - then select the cost item link. This will open a directory window.

The directory is hierarchical. For convenience when large quantities You can create groups of articles, group articles by various signs, by organization (if records are kept for several organizations in one information base). In addition, directory groups can include other groups, thereby creating a multi-level hierarchical structure.

In the new information bases, the directory is filled with default values (predefined elements) for the most common types of costs:

They can be distinguished from articles entered by the user by their icon. It is not recommended to correct or delete them.

Depending on the needs and specifics of the enterprise, users can independently add cost items to the directory (create a cost item in 1C). We recommend that you pay attention that you do not need to enter similar names, as this may lead to incorrect analytics in accounting and “bloat” of the directory.

The cost structure of the enterprise should be thought out in advance, if possible combining small similar expenses into larger groups. It is recommended to enter them into the reference book exactly in the structure in which they are used in reports for economists and managers.

Costs are classified based on the purposes for which the cost is calculated.

Used to analyze the financial results of an enterprise. It differs from classification by item in that all expenses are distributed according to types that characterize their economic content. Each economic element includes an extensive list of articles that are homogeneous in their economic content. For example, the element material costs. It includes items such as raw materials, fuel, tools, etc.

Such a classification makes it possible to determine the cost structure and the share of an individual element in the entire cost. Grouping by economic elements might look like this:

Since in 1C: Accounting 8.3. Since the “Cost Items” directory is hierarchical, you can create groups by economic elements.

However, grouping by cost elements does not allow determining the cost per unit of production. Grouping costs by costing items serves this purpose.

Combines costs based on their place of origin and destination. It is used when preparing cost estimates. The division itself into costing items may be different depending on the purposes of costing. Classification of costs by costing items allows you to determine the cost per unit of production. Grouping costs by costing items can look like this:

Each costing item is entered into the directory as a separate element.

When creating a new directory element in 1C, you must fill in the following details:

Assign a name that reflects the essence of the expense.

Filling out this information is optional. Indicated if hierarchy is used in the directory. In this case, you must indicate which group the article belongs to.

This is a required detail to fill out. Information reflected in given details, used in tax accounting. It is important to correctly indicate the type of cost, because it will reflect tax accounting expenses for income tax purposes. Selected from an existing list that cannot be edited. We focus on the type of expense “Not taken into account for tax purposes.” It is selected if expenses are incurred in accounting and are reflected as expenses, but for the purpose of calculating income tax, they cannot be attributed to expenses that reduce the income tax base.

The details are not required to be filled out. You can specify the document into which this article will be inserted by default. This field can also be left blank.

After entering a new article, it will appear in the directory list.

Already entered cost items can be adjusted or marked for deletion. This should be done with extreme caution due to the fact that this article may have already been used in documents. If you cannot do without adjustments, then after changing the article you should re-enter the documents.

To see how costs are grouped by item, you should generate a report by cost item in 1C 8.3. For this purpose, for example, an account balance sheet or subconto analysis is suitable.

In this article we looked at filling out one of the main and most important 1C directories. Its correct and error-free completion affects the formation of reliable reporting for the enterprise.

The main expenses not accepted for calculating profit, which are often encountered in practice in the operation of an enterprise, are:

All expenses of the enterprise are reflected in expense accounts 20, 23, 25, 26, 44 and in account 91 Other income and expenses.

Data for these accounts in 1C 8.3 is generated based on the correct completion of the Directory of Cost Items and the Directory of Other Income and Expenses.

Let's consider the principle of filling out directories in 1C 8.3 to correctly reflect costs in tax and accounting.

Go to the Directories menu and select Cost Items:

Double clicking opens a list of cost items. If the list has already been fully formed, then the accountant’s task is to check and correct the correct assignment in the directory. Type of expense NU.

For example:

To do this, move the cursor over the Type of NU expense column, use the More button and select the Change function in the list that opens. The list of Types of expenses (NU) opens:

Since the amount of expenses per cost item Notary services beyond the norm cannot reduce the tax base and is reflected only in accounting, we set the Type of expense (NU) – Not taken into account for tax purposes:

In the same way, we check and correct the purpose of all cost items in the column Type of costs of the NU and, in accordance with the norms of Article 270 of the Tax Code of the Russian Federation, set the type of item in the NU - Not taken into account for tax purposes for all expenses not accepted for tax accounting.

Thus, in 1C 8.3, when generating transactions using these cost items in analytics, the expense amounts will be reflected only in accounting.

For example: an employee on a business trip, according to a written order/order from the manager, was paid in excess of the norms established by the order of the enterprise - in the amount of 3,500 rubles. per day. At the same time, the standard travel allowance for the enterprise is 2,000 rubles. per day.

To reflect daily allowances in excess of the norm in accounting, the accountant draws up an advance report in 1C 8.3 as follows:

And when posting the document, we see that in 1C 8.3, for the amount of daily allowance paid according to the norms, entries are generated in accounting and accounting records. And for daily allowances paid in excess of the norm, entries are generated only in the accounting department:

All non-accepted expenses in tax accounting are collected in account N 01.9. That is, this will be the difference between accounting and NU, which will additionally be charged income tax in NU. In short, this means PNO, that is, permanent tax liability.

Cost items in accounting - listThey are formed in the accounting department of each enterprise - they are grouped based on certain principles. The company's accountant has his own main and additional lists of costs, which he pays special attention. What determines their formation and how are they composed?

WITH tax accounting other costs associated with production and sales can be found .

In accordance with section. III PBU No. 10/99 other expenses are not related to ordinary activities. PBU establishes 3 main groups of such expenses.

The first group is associated with types of income from other activities. Such costs arise when a company:

The second group of other expenses is the costs:

The third group is expenses from the occurrence of emergency (force majeure) circumstances.

An enterprise can also classify other expenses by item independently. Here we can recommend the following expense grouping items:

Read the material about calculating variable costs .

The legislation regulating accounting divides all expenses of an enterprise into two large groups: those associated with ordinary activities and other expenses. Expenses associated with ordinary activities are divided into elemental groups. And the enterprise chooses the grouping of expenses by cost items independently. The main and additional lists of cost items are formed full list enterprise costs.

About the accounting procedure individual species costs, read the materials in our section.

In 1C 8.3, the main thing is that the composition of direct expenses is correctly configured in NU, that is, the settings for such correspondence in 1C 8.3 are indicated as part of direct expenses for tax accounting.

Direct expenses in accounting for 1C 8.3 will be those expenses that, when producing or providing services or carrying out work, will be taken into account as a debit to account 20 (23).

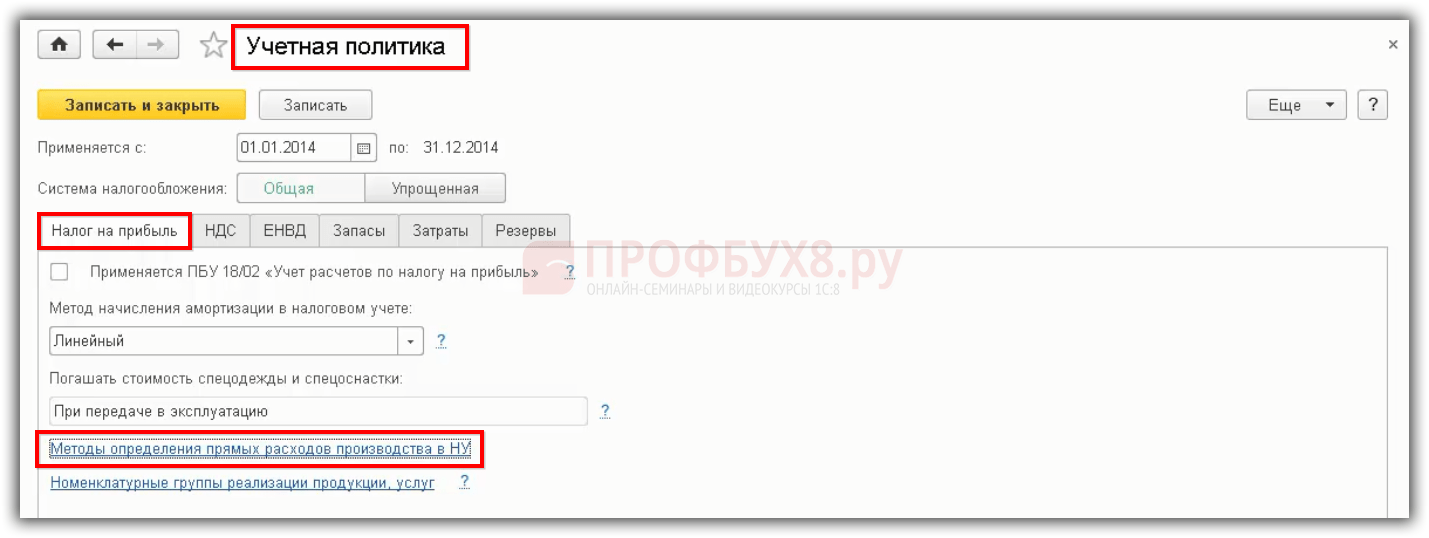

To reflect on the debit side of account 20 direct expenses for accounting in 1C 8.3, you need to set the parameters in the Accounting Policy, on the Costs tab:

It is necessary to indicate with a checkbox the types of activities for which the costs are planned to be taken into account on account 20. The checkbox is checked if direct production costs are taken into account for the production of products and the checkbox is checked for carrying out work and providing services to customers. The checkboxes are checked in order to keep or not keep records of direct expenses in the debit of account 20.

If this expense is direct according to the accounting policy of the organization, then in the transactions in 1C 8.3 you need to reflect the expense on the debit of account 20.

Direct expenses in tax accounting are those expenses, the list of which is reflected in the Accounting Policy. In this case, the list of direct expenses must be specified in the Tax Accounting Policy. This is very important, because this list can be created independently, the Tax Code speaks about this.

To indicate the list of direct expenses in the 1C 8.3 database, there is a setting in the Accounting Policy, which is located in the menu - item Accounting policy– Income Tax tab – hyperlink Methods for determining direct production costs in NU:

In tax accounting, there is no direct dependence on which account in the tax chart of accounts the posting is indicated on.

The principle that if the count is 20, then this is only a direct expense for NU does not apply. The method that is added to “Methods for determining direct costs” is the method that will operate in 1C 8.3:

If for tax accounting expenses are taken into account in the debit of account 26, then in 1C 8.3 it is necessary to make a distribution of indirect expenses for account 26 “In the cost of products, works, services”:

Thus, account 26 is not written off at a time, but is distributed into account 20. This is convenient for those organizations that have decided to bring accounting and tax accounting closer together. When accounts 25 and 26 are distributed to the debit of account 20, that is, the full cost is calculated, it turns out that if account 26 is not defined as part of direct expenses, then the difference will be between accounting and tax accounting. This is normal, and this is what is expected by law.

Account 44 cannot be specified in “Methods for determining direct expenses”. Even if you add 44 accounts, the 1C 8.3 program will not define it as a direct expense. Also, if account 26 is added to the “Methods for determining direct expenses”, but in the Accounting Policy parameters the distribution of indirect expenses using the direct costing method is set, then account 26 will not be defined as a direct expense. Only if accounts 25 and 26 are distributed to the debit of account 20 and a list of direct expenses is specified, then everything will work in 1C 8.3.

To automate the correct process, it is important that the list of expenses is approved in accordance with the organization’s Accounting Policy.

In the Income Tax Declaration, direct expenses are reflected in Sheet 02 of Appendix 2, in lines 010, 020. It is for line 010 that the list of direct expenses is formed:

Those expenses that will be indicated in the “Methods for determining direct production costs in NU”, those expenses will be included in the income tax return. If the declaration is incorrectly formed, the calculation of income tax will be considered inconsistent with reality.

Let's consider whether in 1C 8.3 it is possible to implement automatic write-off of expenses from account 20 without taking into account revenue by item group.

- this is a type of goods, works and services in 1C 8.3.

In the 1C 8.3 database there is, where there is a group Products - these are the final products of the organization:

Or there is such a group as Services, which has its own services, that is, those services that are provided directly to customers:

In 1C 8.3 there is a directory Nomenclature groups. Many 1C 8.3 users are confused about what they are needed for. It seems that there is a nomenclature that is inserted into the documents for implementation. But in 1C 8.3 there are item groups for which analytical accounting is maintained on account credit 90, that is, both the item and the item group are added to revenue. The debit of account 20 is accumulated specifically according to the item group:

In the previous version of the 1C 8.2 program, until the revenue passes through the item group, account 20 will not be closed. For this reason, problems arose with, because for some services there could either be no revenue or, for example, sales are carried out in one product group, and costs are reflected in two lines.

In order to avoid difficulties with closing account 20, 1C developers introduced a parameter in the Accounting Policy settings to close account 20 without taking into account revenue. This setting must be used for work or services:

Thus, in 1C 8.3 the Accounting Policy provides options for closing account 20 for works and services at the end of the month:

In 1C 8.3, this method makes it easier to work with 20 counts. If in 1C 8.3 it is difficult to maintain the dependence of account 20 on the credit of account 90 and item groups, then this method is the most acceptable, and account 20 will be closed monthly.

According to this method, the debit of account 20 will be closed if there is no revenue on the credit of account 90 or the revenue comes from another item group, provided that the Accounting Policy specifies the method for closing account 20 - “Without taking into account revenue from work.”

Thus, all costs recorded on account 20 for work and services will be written off automatically in full in Dt 90 always at the end of the month. Regardless of whether the proceeds from loan 90 are reflected or not reflected.

To this method reflect “ ”, in 1C 8.3 you need to enter the document “Inventory of work in progress”, then the debit of account 20 will be closed minus the amount of “work in progress”:

If in 1C 8.3 the option for setting up the Accounting Policy “Taking into account revenue from work” is selected, then

Thus, strict compliance is necessary so that the debit of account 20 reflects the costs of one item group and the revenue necessarily goes through this item group. If there is no revenue for the item group in the current month, then account 20 will not be closed and will be transferred as “unfinished” to the next month.

Entered using the document “Provision of production services”. In this method:

Thus, if there is a debit to account 20 for a certain item group, then in order for it to be closed, revenue must be reflected for the same item group on the credit of account 90.01 using the document “Provision of production services.” You cannot use other documents for the sale of goods and services, otherwise the account will not be closed.